Wir Sind Keine Berliner!

In June of 1963, twenty- two months after East Germany had erected the Berlin wall to prevent emigration to West Berlin, President John Kennedy came to Berlin and delivered one of the most famous speeches of the Cold War:

Two thousand years ago, the proudest boast was “civis romanus sum” (I am a Roman citizen). Today, in the world of freedom, the proudest boast is "Ich bin ein Berliner!"... All free men, wherever they may live, are citizens of Berlin, and therefore, as a free man, I take pride in the words "Ich bin ein Berliner!" [1]

Kennedy declared “ich bin ein Berliner” (I am a Berliner) to show that the longing for freedom transcended national boundaries, and that he and all the free peoples of the world supported Berliners in their struggle against communist oppression.

Today, Germans suffer under a different oppression – the economy-killing dictates of the Decarb Dreamers – that has created a green wall between German industry and affordable energy, causing a seemingly interminable recession. Unfortunately, many in the U.S. seem determined to take America down this same path.

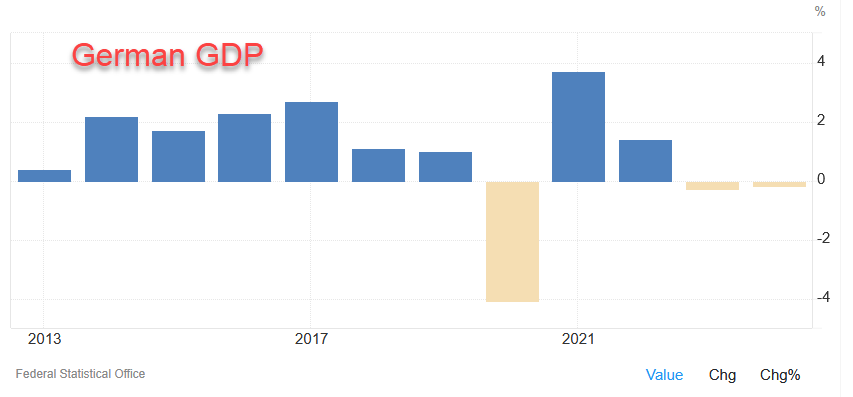

Coming out of the Covid recession in 2020, German GDP grew for 2 years and then slumped in 2023 and 2024.[2] Manufacturing saw a significant drop in output, along with trade, transport and accommodation in the service sector. Capital formation also fell, particularly in construction and machinery.

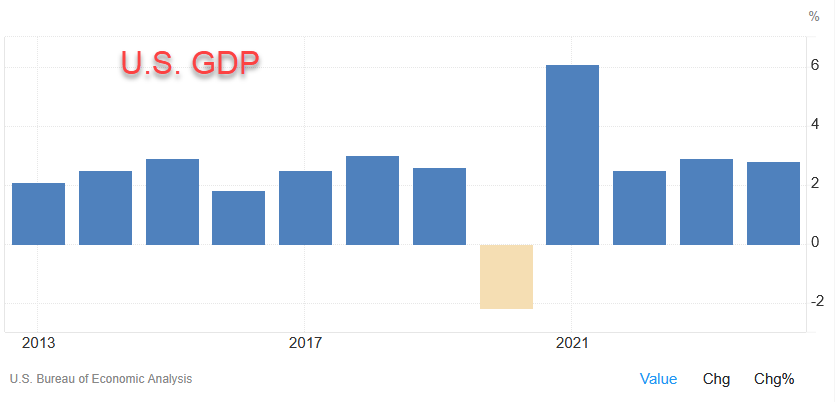

This contraction was a German phenomenon; during this same time period the U.S. enjoyed moderate growth.[3]

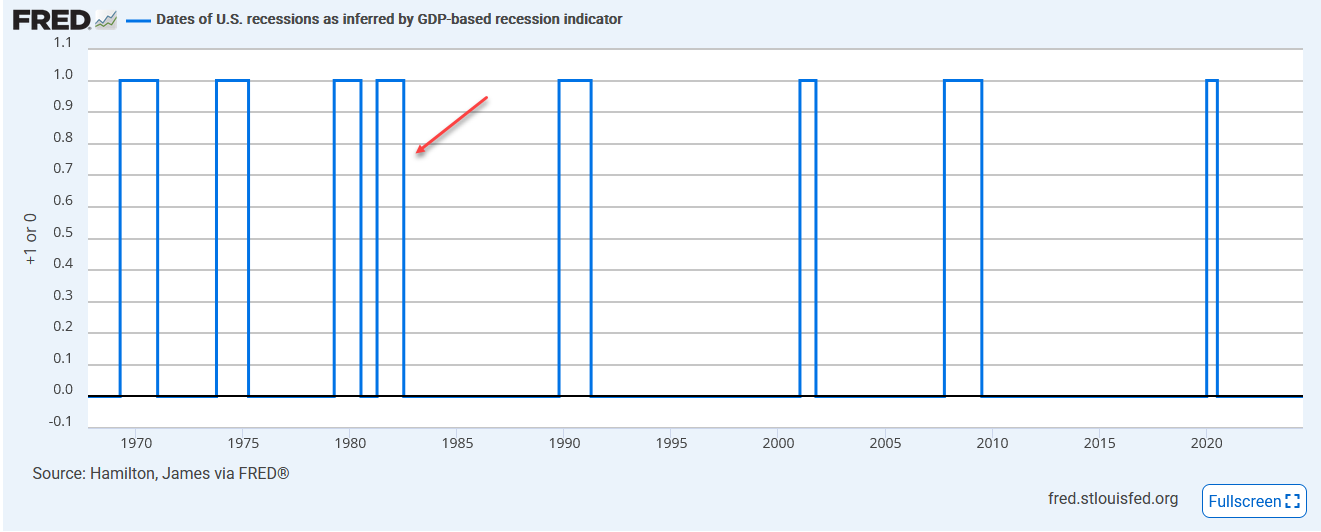

I labeled Germany’s economic woes “seemingly interminable” because the closest thing we have seen to this in the last 55 years were the inflation-induced spasms of the 1970’s, which culminated in the double-dip downturn that lasted from the 2nd quarter of ’79 to the 3rd quarter of ’82.[4] An economic downturn that lasts 2 years or more, though not exactly a black-swan event, is still very unusual.

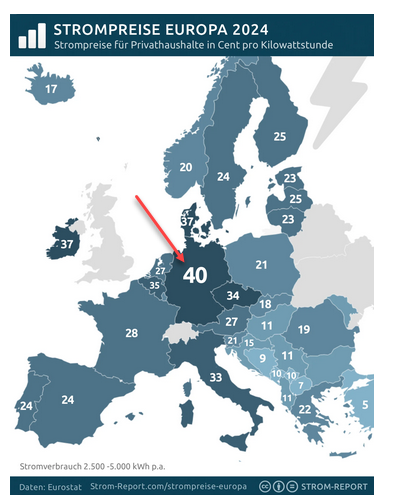

How has Germany become the latest “sick man of Europe?” Though analysts debate the impact of a number of factors – demographic shifts, the weakening auto industry, digitalization, protectionism, limits on public borrowing[5] -- almost all agree that astronomical energy costs are throttling Germany’s economy; Germany now has the highest energy costs of any European country.[6]

Why are German industry and consumers so burdened? The answer, for those who have even a passing familiarity with energy reality, is simple: decarbonization.

The German government likes to crow about how they have almost reached renewable heaven, but the invaluable Francis Menton has dug into the numbers and revealed that what appears to be the inevitable march of progress is more like the spinning of a hamster on a wheel. In 2023, 43.6% of the country’s electricity consumption came from wind and solar. In the first 6 months of 2024 that number increased to 43.9%, a paltry rise of .3%. But between year-end 2022 and year-end 2023, its solar generation capacity rose from 67.6 GW to 79.2 GW, an increase of more than 17%, and its wind generation capacity went from 66.1 GW to 68.8 GW, an increase of over 4%.[7]

This means that in 2022 and 2023, the Germans sunk an enormous amount of capital into wind and solar, but in 2024 only managed to create a miniscule increase in its usage. This is a proven recipe for a recession, well understood since the days of Adam Smith. Economic growth is fueled by productivity growth, which is the result of processes that allow us to create more from less. Deutschland is now creating less energy with more input, a classic case of growth-stifling malinvestment.

The Wall St. Journal sums it up nicely:

Blame a green-energy transition that’s been under way for some 20 years. Germany has steadily removed affordable mainstays such as coal from its power mix, while also phasing out dependable nuclear power. Russia’s 2022 invasion of Ukraine heightened the contradictions of the energy transformation. The economy had come to rely on cheap Russian natural gas to offset all Germany’s other energy expenses. With that stopgap no longer available to the same degree, nothing shields the German economy from Berlin’s energy mistakes. Result: two years of recession and accelerating deindustrialization.[8]

And it looks like there is no end in sight to this deindustrialization death spiral. None of Germany’s political parties – left, center, right – will acknowledge the green roots of the problem, and consequently the country is enduring an election campaign about who can better administer the transition to renewables, when the debate should focus on ending the transition. [9]

With the ascendance of Trump II, and his withdrawal of the U.S. from the Paris Climate Agreement and his freeze on green energy funding, it would appear that America is returning to energy sanity, but many states seem determined to follow Germany and dig their green holes deeper.

Though California reduced its climate change spending by 7% last year because it had run through its budget surplus, it still earmarked $48.3 billion for a vast array of programs such as EV subsidies, funds for making the coast more resilient, wind and solar projects, and securing water supplies and preparing for wildfires. (Though it looks like spending on water and wildfire prevention may have been neglected just a bit!)[10]

New York Governor Kathy Hochul now finds herself in a similar head-in-the-sand position as the German politicians who refuse to acknowledge the role green energy has played in their country’s doldrums. Recently, Con Ed, which serves greater New York City, proposed an enormous rate increase. Former New York Public Service Commission member John Howard blamed this increase on the cost of “clean” energy.[11] Hochul responded by urging the PSC to reject the rate hike and audit the salaries of utility employees,[12] without mentioning the effect of her renewable energy policies.

It is not just state governments that are declaiming Ich bin ein Berliner when it comes to foolish energy policy. Many U.S. mutual fund managers also seem determined to ignore the portent of Germany’s experience.

The Net Zero Asset Manager’s Initiative (NZAM) is an international group of asset managers committed to the goal of net zero greenhouse gas emissions by 2050 or sooner. After Blackrock and other major players recently withdrew from the initiative,[13]NZAM suspended operations, but investment managers such as T. Rowe Price continue to invest their clients’ money in accordance with the principles that are destroying Germany’s economy. As of 12/31/23, T. Rowe had committed 61% of its assets under management to net zero,[14] and even after the shuttering of NZAM, they soldier on:

Our commitments to the Net Zero Asset Managers initiative (NZAM) . . . were made prior to the decision by NZAM, on 13 January 2025, to launch a review of the initiative. Notwithstanding, T. Rowe Price remains committed to offering our clients net zero and climate-related investment solutions that meet their needs, in line with our fiduciary responsibilities.

The commitments we have made as signatories of NZAM are entirely in line with our fiduciary responsibility and there is no change to our existing investment process. At T. Rowe Price, climate transition is considered as part of our ESG analysis and integrated into our fundamental research and portfolio construction where appropriate.

We expect our committed assets to increase over time as data coverage improves, net zero methodologies for asset classes such as sovereign bonds get developed, and we launch net zero products.[15]

Clearbridge, in its 2025 ESG Outlook: Sustainability as a Business Driver,[16] seems to have missed Germany’s struggles with renewables. In spite of the Germans’ economy-killing embrace of wind and solar, Clearbridge believes that the deceptively labeled Inflation Reduction Act -- essentially a climate change bill[17] -- will somehow “compound economic growth.” They assume that the “energy transition is a global reality,” ignoring Francis Menton’s analysis cited above that shows that in Germany, this so-called transition has run itself into a green dead end in which the massive build out of wind and solar has barely created a thimbleful of increased consumption from renewable sources.

From state governments to major investment managers, many U.S. institutions seem hell bent on sucking the light and life out of America’s energy supplies and forcing us down Germany’s dark and dismal path.

There is a good chance that many of these Decarb Dreamers admire President John F. Kennedy, Jr. without realizing that in all probability, he would be adamantly opposed to their net-zero suffocation of the U.S. economy. He was a champion of economic growth, as evidenced by the speech he gave to the Economic Club of New York in December of 1962, in which he argued that his tax cuts would boost prosperity.[18] And in September of 1963, he made a 10,000 mile, 11-state, five day journey through the American West to review the region’s natural resources, with the highlight of the trip being a speech at the Hanford Reactor in Washington State in which he extolled the virtues of “low cost atomic power.”[19]

I believe that if JFK were alive today, he would proudly proclaim “Wir sind keine Berliner!” – “We are not Berliners!”

Don Harrison

Every investor’s situation is unique and you should consider your investment goals, risk tolerance, and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. Investing involves risk and you may incur a profit or loss regardless of strategy selected, including diversification and asset allocation.

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Don Harrison and not necessarily those of Raymond James.

[1] https://en.wikipedia.org/wiki/Ich_bin_ein_Berliner

[2]https://tradingeconomics.com/germany/full-year-gdp-growth

[4] https://fred.stlouisfed.org/series/JHDUSRGDPBR

[5]https://www.euronews.com/business/2024/12/24/five-major-economic-hurdles-germany-needs-to-overcome-in-2025

[6] https://strom-report.com/strompreise-europa/

[7] https://wattsupwiththat.com/2024/09/08/in-germany-the-energy-transition-situation-only-gets-worse/

[8] https://www.wsj.com/opinion/germanys-election-dodges-its-climate-debacle-scholz-merz-cdu-3387ef24?mod=opinion_lead_pos7

[9] https://www.wsj.com/opinion/germanys-election-dodges-its-climate-debacle-scholz-merz-cdu-3387ef24?mod=opinion_lead_pos7

[10] https://calmatters.org/environment/2024/01/newsom-plan-cuts-california-climate-funding/

[11] https://nypost.com/2025/02/05/us-news/con-ed-proposes-massive-rate-hikes-that-could-send-new-yorkers-gas-electric-bills-soaring-thanks-to-hochul/

[12] https://www.governor.ny.gov/news/keeping-money-your-pockets-governor-hochul-takes-sky-high-utility-costs-and-demands

[13]https://www.ipe.com/news/net-zero-asset-managers-initiative-halts-activities/10128152.article#:~:text=Net%20Zero%20Asset%20Managers%20initiative%20halts%20activities,removing%20its%20net%2Dzero%20targets%20and%20member%20obligations.

[14] https://www.troweprice.com/corporate/us/en/what-we-do/esg-approach/journey-to-net-zero.html

[16] https://www.clearbridge.com/blogs/2024/2025-esg-outlook-sustainability-as-a-business-driver

[17] https://www.epi.org/blog/the-inflation-reduction-act-finally-gave-the-u-s-a-real-climate-change-policy

[18] https://www.americanrhetoric.com/speeches/jfkeconomicclubaddress.html

[19] https://www.historylink.org/file/10640